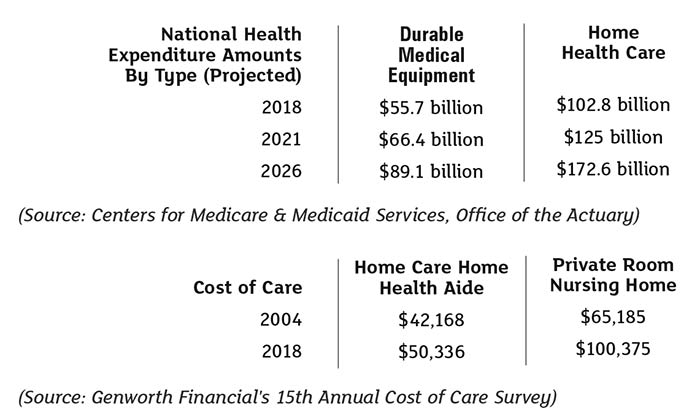

Most owners of a durable medical equipment (DME) company can readily estimate the value of their company. Unfortunately, their estimates are usually wrong. Common threads among DME company owner valuation statements include: “All DMEs sell for two times annual revenue,” or “My DME should be worth the sum of all of the monies I invested into the company,” or “I wouldn’t consider selling my DME for less than 10 times annual profits.” Those who make these statements are in for a rude awakening when they attempt to sell their company or engage a skilled health care valuation professional. Although most owners of DME companies are pretty smart, the value they have in their head for their company is almost always incorrect. Here’s why:

Bottom Line

- DME company owners underestimate the riskiness of their company and consequently over-value their company. Small private companies are significantly riskier investments than large public companies.

- Owners sometimes estimate value based on how much they have invested in their company. However, the amount of money invested in a company may have no bearing on the current value. (Remember Time Warner’s investment in AOL?)

- Owners might estimate value based on market multiples that they’ve heard from other business owners, known as “Country Club Multiples.” Beware of Country Club Multiples, as Mark Twain quipped, “There are three kinds of lies—lies, damn lies and statistics.”

- Owners are often too emotionally attached to their company to see its value from an outsider’s perspective (i.e., dispassionately). As such, they overestimate the amount buyers are willing to pay for their company.

- Owners are typically overly optimistic during economic good times and overly pessimistic during economic hard times. As such, they overestimate their company’s potential and value during a prosperous economy.

- Owners overestimate how long they plan to continue running their company. As such, they think about company value in terms of the future, not the present.

- Owners may have used online business valuation calculators to estimate the value of their company. Unfortunately, those online business valuation calculations are notoriously inaccurate.

Ultimately, the value of any company is how much someone else is willing to pay to own it. As business valuators, the best we can come up with is an estimate of market value. Although there are numerous valuation methods, the most prevalent that are used to value going-concern businesses are the comparable transaction analysis (market approach) and discounted cash flow analysis (income approach).

What is discounted cash flow analysis (income approach)?

A more reasonable estimation of value can be determined using a discounted cash flow analysis where future cash flows are projected and “discounted” back into today’s dollars. For example, if a company is expected to earn $500,000 a year in cash flow for the foreseeable future, the value of the company would be $2,000,000, assuming a discount rate of 25 percent.

The challenge with the discounted cash flow analysis (income approach) is accurately projecting future company cash flows and accurately determining the discount rate. The discount rate should reflect the riskiness of the company. Most company owners underestimate the riskiness of their company. For example, an owner of a small, privately held company once told me that his company was no riskier than industry-related companies on the S&P 500 index.

What is comparable transaction analysis (market approach)?

A reasonable estimation of value can be determined by looking at past sale transactions of comparable companies. For example, if you found 20 companies of similar revenue and earnings that sold for four times EBITDA (earnings before interest taxes, depreciation and amortization), you might compare those past sale transactions to your EBITDA. You might also compare the sale price of the past transactions to annual revenue of those companies, and compare the same percentage to your company’s annual revenue.

The problem with the comparable transaction analysis (market approach) is that it assumes all companies in an industry are the same. What if your company is growing faster than the industry average? What if your company specializes in new technologies, while the comparable transaction companies were not tech savvy? What if you have true rainmakers? Truly comparable transactions may be hard to find.

The Market Multiples (Valuation) graphic above contains current market values of DME companies. Note that the actual market value of your specific DME company may differ from the multiples in the graphic based on other factors, noted below.

Factors that Affect Valuation

- No rainmaker dependence. No dependence on a single rainmaker that drives the majority of referrals. Rather, have a balance of key employees, varied referral sources, multiple vendors and several professional service providers.

- Healthy diversity of services. DME company owners should consider offering various services to reduce revenue volatility, such as complex rehab therapy (CRT), clinical respiratory, home modifications, managed care, home health care, wound care and hospice managed care.

- Increased growth opportunities. Scalability is a key factor that attracts buyers and investors in the DME marketplace. Growing demographics, emergent brand awareness, new markets, new/improved service offerings, and the ability to quickly respond to changing payer requirements create buyer excitement.

- Favorable payer mix. A diverse payer mix may consist of Medicare, Medicaid, commercial insurance, B2B and cash pay.

- Significant company size. As company revenues increase, so do the number of potential buyers and, accordingly, market value.

- Solid financial performance. Company performance ratios greater than industry averages indicate a well-run organization. Well-run DME companies will often have net profit margins in the 7 to 12 percent range.

- Favorable local demographics. DME companies located in regions with a growing population, aging population or emerging middle class provide for favorable revenue growth.

- Recent billing/compliance audit. Having a recently completed billing audit conducted by an outside billing consultant will decrease buyers’ perception of company risk and thus increase value.

Bottom Line

The value of your DME company is based on many factors, such as your payer mix, local demographics, quality and tenure of staff, quality of referral sources, product mix, quality of vendors and marketability of existing inventory. Ultimately, your DME company is worth what someone is willing to pay for it.