Home health entities are impacted—as are all businesses—by myriad tax law changes introduced in the Tax Cuts and Jobs Act (TCJA), passed in December 2017. One of the most complex provisions is the deduction related to pass-through entities, also known as Section 199A.

Determining the deduction includes a matrix of complicated calculations. (Figure 1 helps demystify the general concepts and income levels that determine the application of the deduction.)

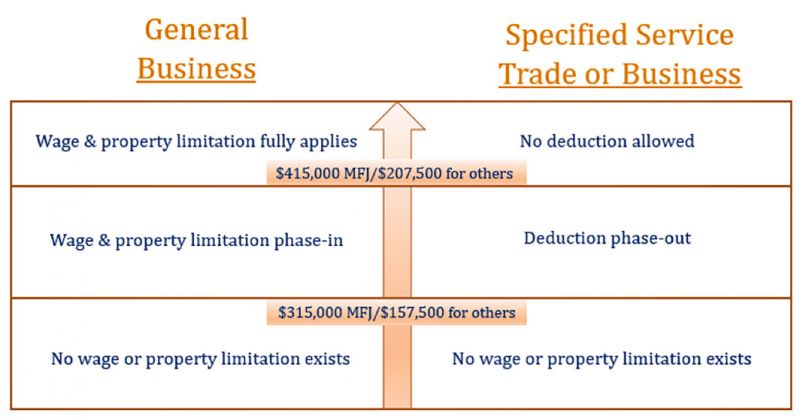

Figure 1. Determining the pass-through deduction

Figure 1. Determining the pass-through deductionThe overarching question for home health: What is general business?

General business in the TCJA is defined as “qualified trade or business” that generates qualified business income (QBI) for the pass-through deduction. Income qualifying for this deduction includes the QBI of proprietors, partners (including LLC members), and S corporation shareholders. Health care is listed as an excluded trade or business for determination of QBI. As such, health care entities fall into the dreaded category of specified service trade or business (SSTB).

In August 2018, the U.S. Department of the Treasury issued 200 pages of proposed regulations interpreting the Section 199A provisions. Included is clarification and guidance related to the vague terminology “the field of health.” The definition provided some clarity for professionals specifically named:

The Field of Health includes the provision of medical services provided by physicians, nurses, therapists, psychologists and other similar health care professionals performing services provided directly to a patient.

The “field of health” does not include services not directly related to a medical services field, even though the services provided may purportedly relate to the health of the service recipient.

The proposed regulations do not expressly address certain types of businesses that may not “provide medical services directly to a patient.”

The proposed regulations provide examples that may help determine if an entity is eligible for the Section 199A deduction. One health care example involves a dermatology practice that sells skincare products to its patients. The products are sold in the same space as the dermatology practice and by the same employees who work for the dermatology practice.

In the example, the gross receipts for the skincare products are only 5 percent of the entity’s overall gross receipts. Although the sale of skincare products is not “the performance of services in the field of health” as defined in the proposed regulations (since the gross sales are minimal and the services are co-mingled with the practice), they are considered an incidental service and excluded from the Section 199A deduction.

If the skincare products were sold in a separate business, with a separate lease and employees, would it be classified as an SSTB? Dissecting the definition may provide some guidance: Home health does “provide medical services” by “nurses” “directly to patients.” But the final determination will depend on a careful analysis of the facts and circumstances in light of a complex set of factors.

The proposed regulations also address anti-abuse rules. Any trade or business that provides 80 percent or more of its services to a 50 percent commonly owned SSTB will be treated as an SSTB. The regulations include an example of a law firm attempting to spin off its administrative services into a separate LLC. In the example, there is 50 percent common ownership and all services are provided to the law firm, resulting in the LLC being classified as an SSTB. The same result would apply to home health entities that have management companies with 50 percent common ownership that provide billing services solely for the medical practice.

However, if an SSTB owner’s taxable income is below $315,000 (married filing jointly) or $157,500 (all others), they qualify for the 20 percent deduction. The deduction phases out between $315,000 to $415,000 for married filing jointly and $157,000 to $207,500 for others.

This is a deduction taken on the owner’s individual income tax return (Form 1040). It does not reduce self-employment income or net investment income, but it is a deduction for alternative minimum tax purposes. You do not have to itemize your deductions for this.

Summary

The 200 pages of proposed regulations cannot be completely addressed quickly or easily, and this component of the tax law change is complex and fraught with intricate calculations and interpretations. The best advice is to tread carefully and seek counsel from a tax professional.