External factors that fundamentally impact this sector of health care

Thursday, October 27, 2016

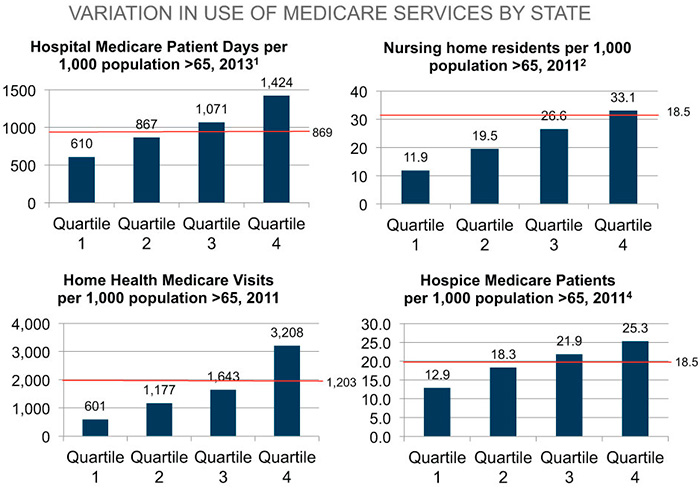

In this article, Alvarez & Marsal (A&M) provides a brief synopsis of the external factors that will fundamentally alter the post-acute sector. These include a rapidly aging population; health system and hospital consolidation, the evolution of Medicare payment reform; a preference by many state Medicaid agencies for homecare based services; The Impact Act of 2014; and the advent of “Big Data.” The magnitude, rate and timing of change will vary by state, and more specifically, metropolitan statistical area based on the local supply and demand for services, as well as competitive intensity.

Historically, post-acute care stakeholders have benefitted from a facility-centric reimbursement system. That will change, as United States Department of Health & Human Services (HHS) Secretary Sylvia Burwell has stated her objective to have alternative payment models account for 50 percent of payments by 2018, and to have quality and value metrics linked to 90 percent of all Medicare fee-for-service payments by the same year.